Outlook

January 20, 2026

2025 ended with markets near all-time highs and the S&P 500 gaining +17.9%. The bull market marched on during a choppy fourth quarter as it climbed a wall of worry with the S&P 500 ending up +2.7%. Volatility was driven by the US government shutdown and its impact on economic visibility as it became difficult to assess the economy due to the delayed release of key reports on employment, inflation, spending and activity. November and December saw additional pressure due to the AI narrative being questioned as well as year-end rebalancing and tax loss selling. Ultimately, positive underlying trends persisted and markets regained their footing, supported by earnings, rate cuts and the eventual release of strong economic data.

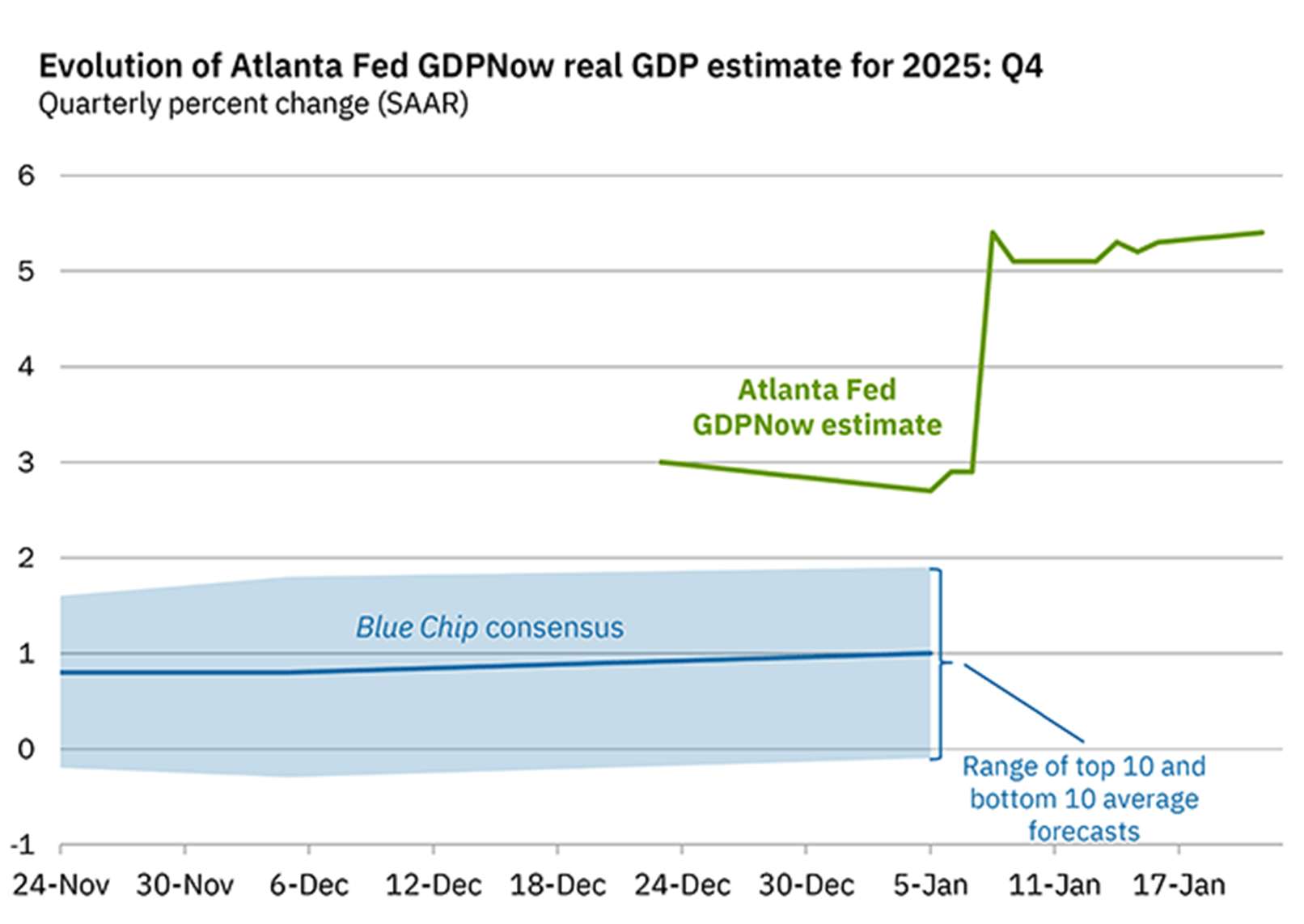

The U.S. economy continues to be robust and is growing above trend, powered by expansive fiscal policy, dovish monetary policy, a productivity boom and the surge in artificial-intelligence investment. In the third quarter, U.S. GDP grew 4.3% (not released until January due to the gov shutdown), driven by personal consumption and domestic investment growth. ISM and S&P Global’s Manufacturing and Services PMI and Retail Sales continue to be supportive. NFIB Small Business Optimism Index is persistently optimistic. The Atlanta Fed’s GDPNow model is now estimating real GDP of +5.4% for Q4 (Chart 1).

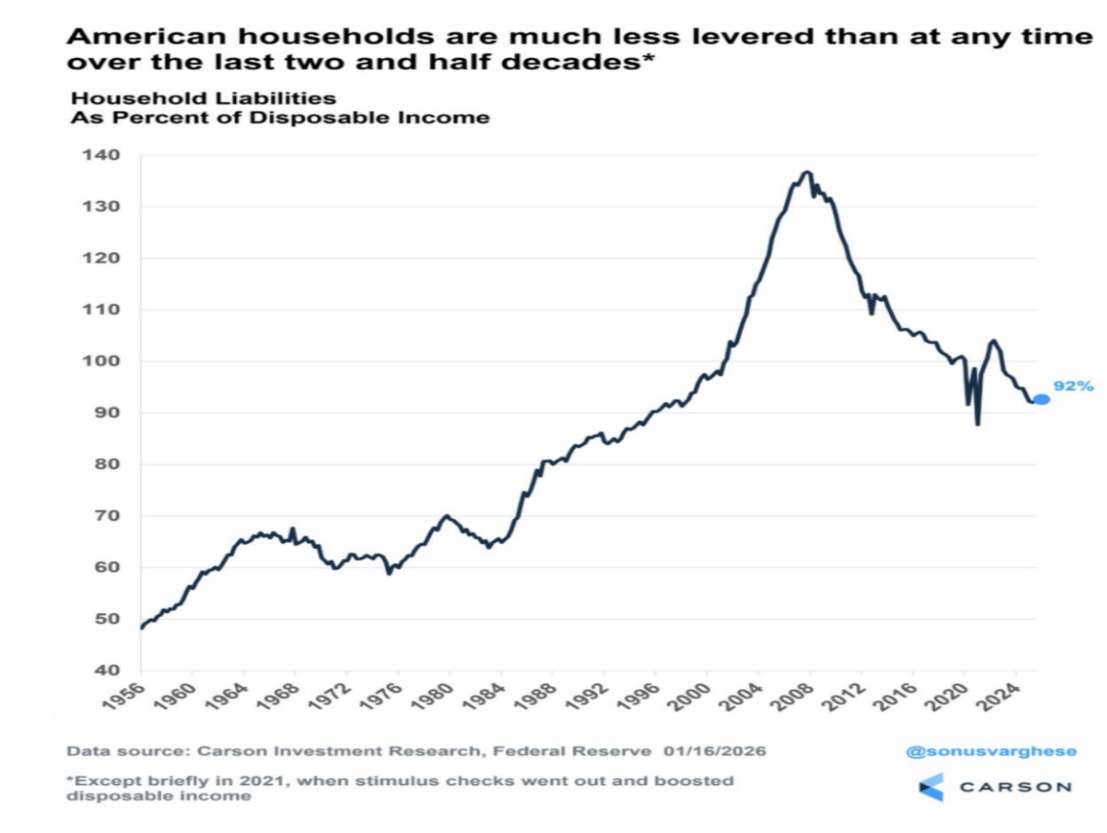

The US labor market continues to be uncertain but relatively stable. Weekly initial jobless claims continue to report in a tight range around 215k as they have for the last few years. Net Non-Farm Payrolls are averaging ~50k a month since May following the significant shift in immigration. The unemployment rate was 4.4% in December, down from 4.5% the prior month. Productivity continues to boom. Job market concerns have created sufficient doubt to keep exuberance in check, resulting in consumer sentiment remaining low, but spending remains resilient. Household balance sheets remain healthy (Chart 2) and there will be a boost coming from tax refunds because of the retroactive tax bill passed last year.

Inflation continues to be in a downtrend, but the pace of improvement remains slow. Tariffs and shifting supply chains have not been as negative as initially feared. Consumption is resilient, but not enough to pressure prices higher. The slow pace of rate cuts has been balanced with the soft labor market. Like employment, this relationship remains stable, but a deviation would be concerning.

The Federal Reserve continued easing by cutting rates 25bps in October and again in December. These cuts continue to be framed as insurance against labor market softening rather than concerns over inflation or imminent stress. Two additional 25bps cuts are projected for the back half of 2026. Jerome Powell’s term as Chairman will end in May of this year and policy is likely to remain on hold for now. Trump’s nominee for the Fed Chair is expected to favor looser monetary policy, but a significant shift is unlikely without clearer deterioration in jobs or inflation. Either way, monetary policy remains in an easing phase, supporting growth.

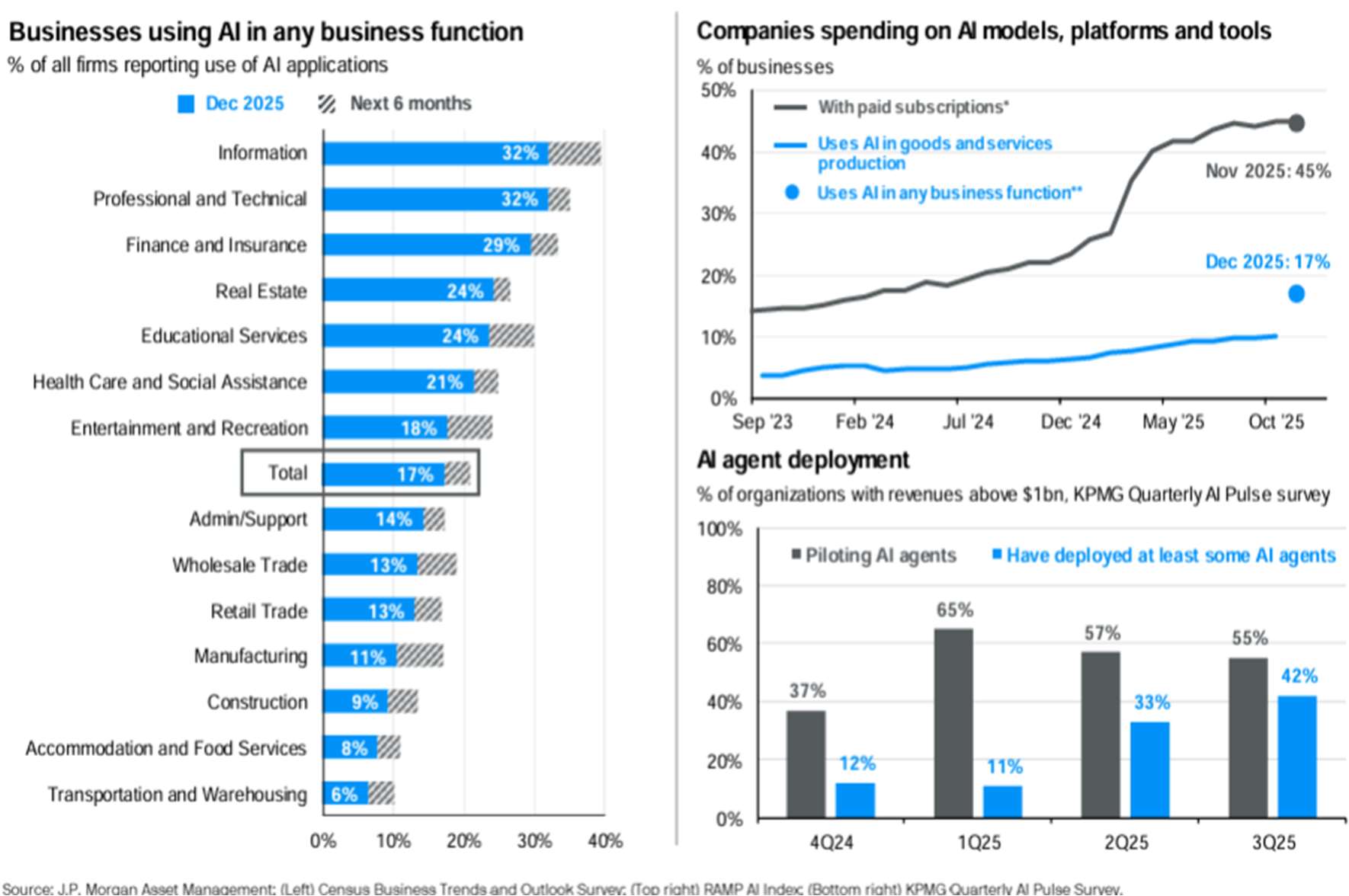

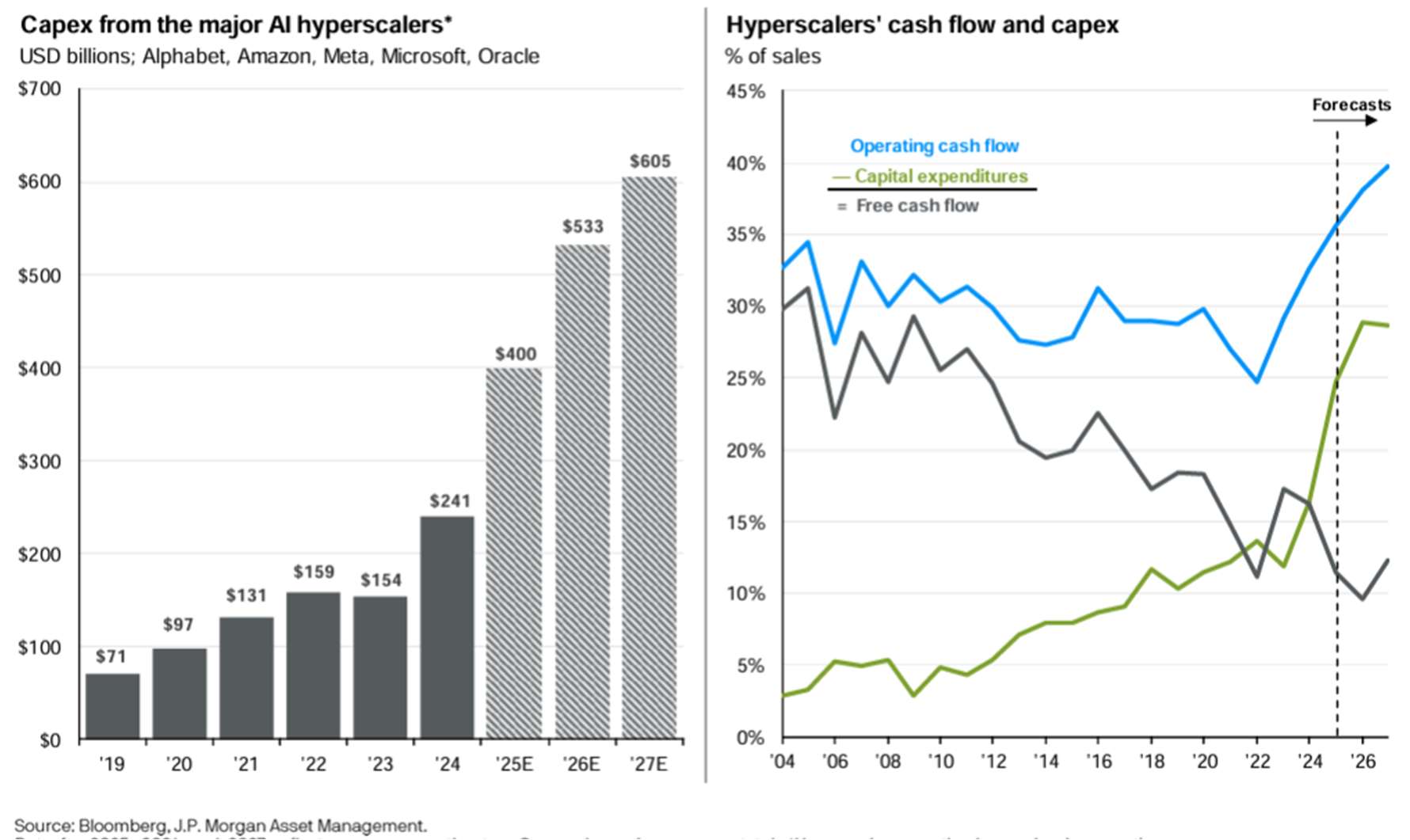

AI remains the dominant theme and growth driver for markets. However, after months of strong gains fueled by AI enthusiasm, investors questioned whether the rapid rise was sustainable, causing a major reset in November. Skepticism mounted about excessive AI spending, data-center buildouts and whether profits would ever justify the spending. While this capital expenditure cycle does have parallels to bubbles of the past, there remain notable differences. The length of this cycle is very short, only a few years, with technology acceleration and broad adoption significantly faster than in the past (Chart 3), and most importantly funding is primarily coming from cashflows (Chart 4). Low relative debt levels suggest we’re not in the latter part of the cycle. Finally, the supply constrained nature of semiconductors and energy will continue to keep overbuilding in check. While this theme could ultimately become a problem, this is unlikely to play out in 2026 or even 2027.

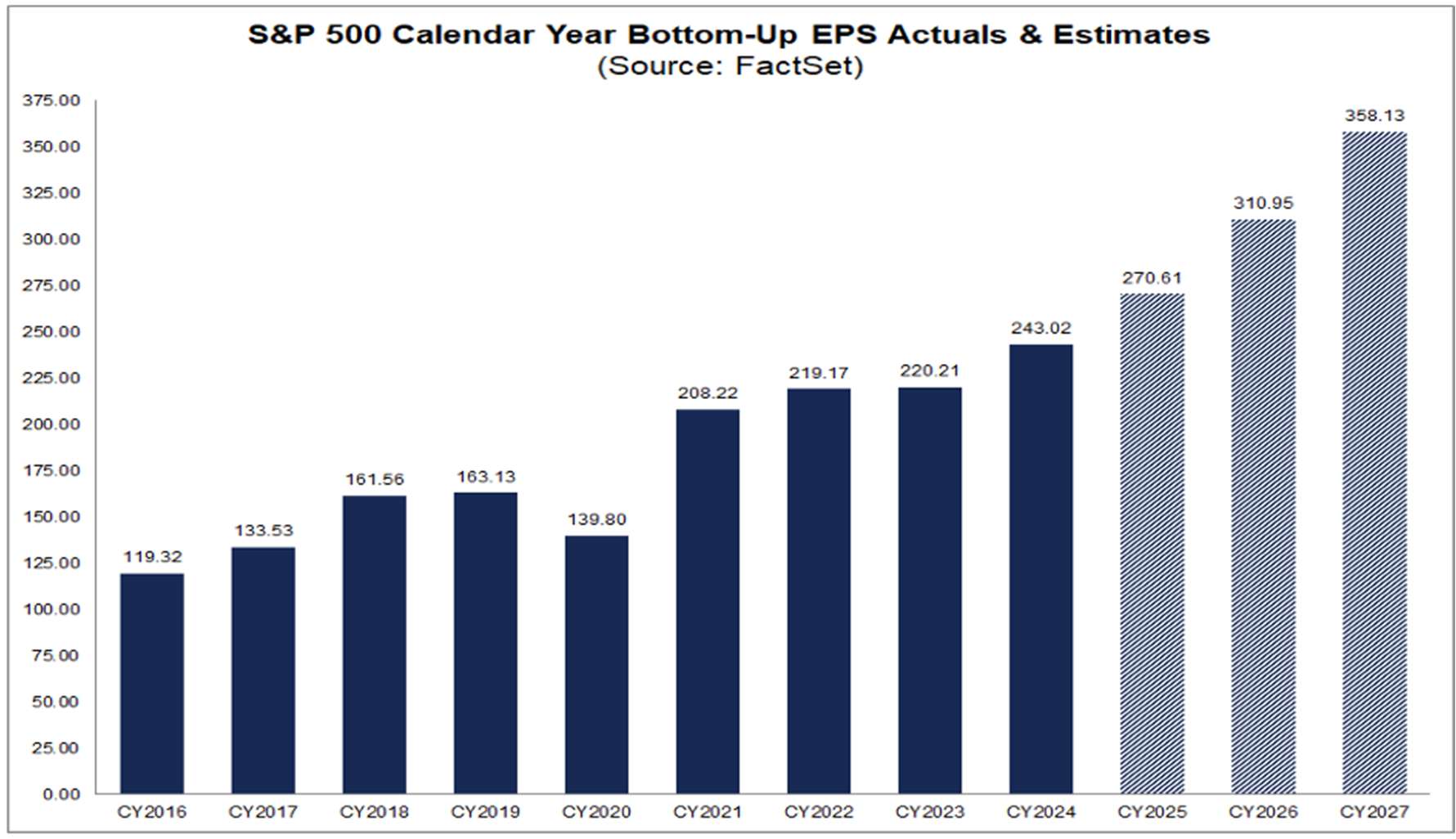

For Q4 2025, according to FactSet’s January 16th Earnings Insight, the estimated year-over-year earnings growth rate for the S&P 500 is now +8.2%, the tenth straight quarter of growth. Revenue is expected to grow +7.8%, the second highest rate since 2022 and the 21st consecutive quarter of growth. Expectations continue to support acceleration through 2026 and with breadth improving. For Q1 2026, analysts are projecting earnings growth of 12.2% and +14.9% for the calendar year (Chart 5).

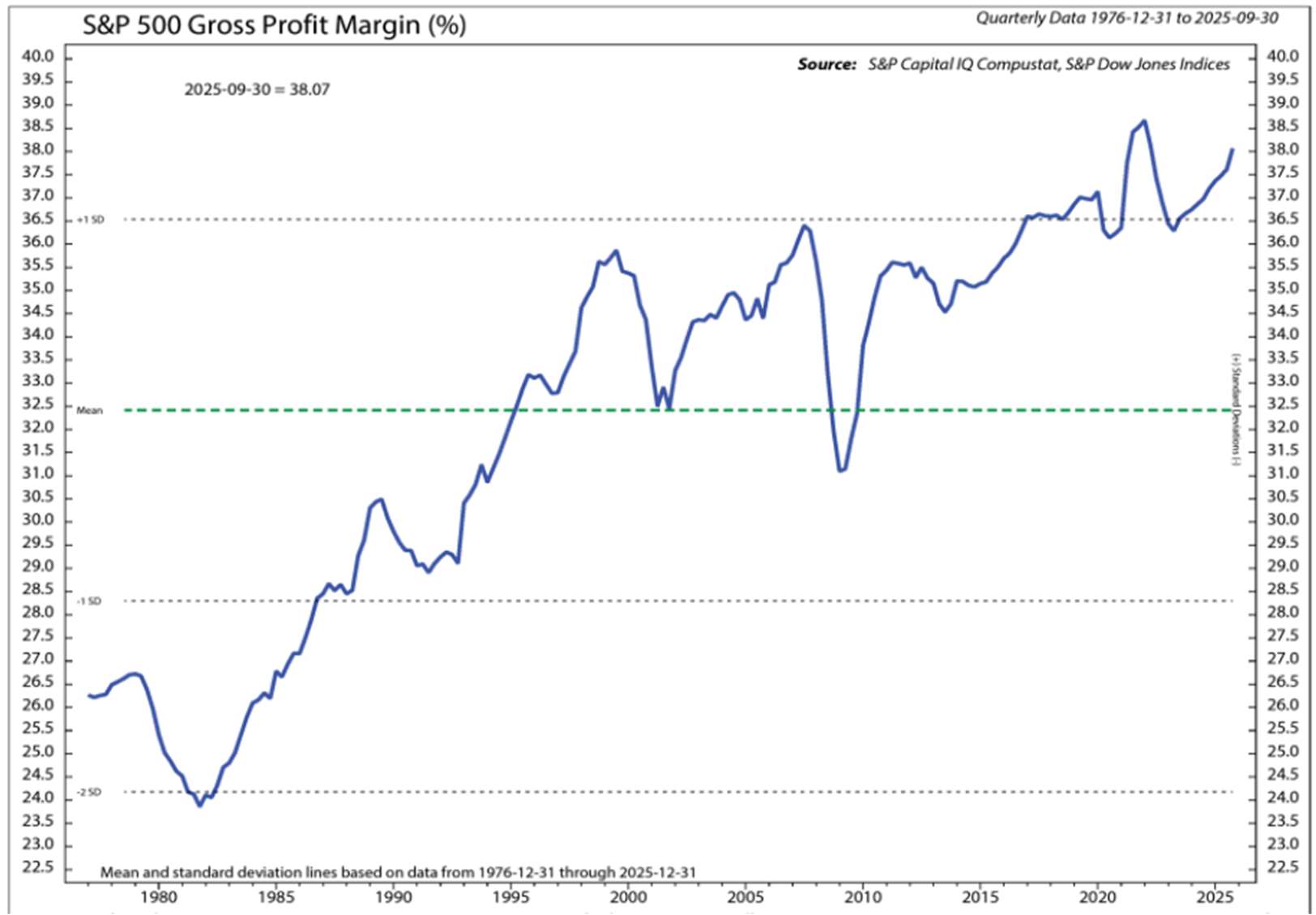

Valuations continued to be full but remained at the same level as at the end of the third quarter and end of the year. Rising earnings have kept up with rising prices and prevented further elevation. Margins trends remain strong, supporting high valuations (Chart 6). The forward 12-month P/E ratio for the S&P 500 is 22.2. In the short term, a subsequent move higher for the market will depend on continuation of the earnings tailwind to earn the multiple. The 12-month, bottom-up target for the S&P 500 is now 8084, 16.4% above Friday’s closing level of 6,944.

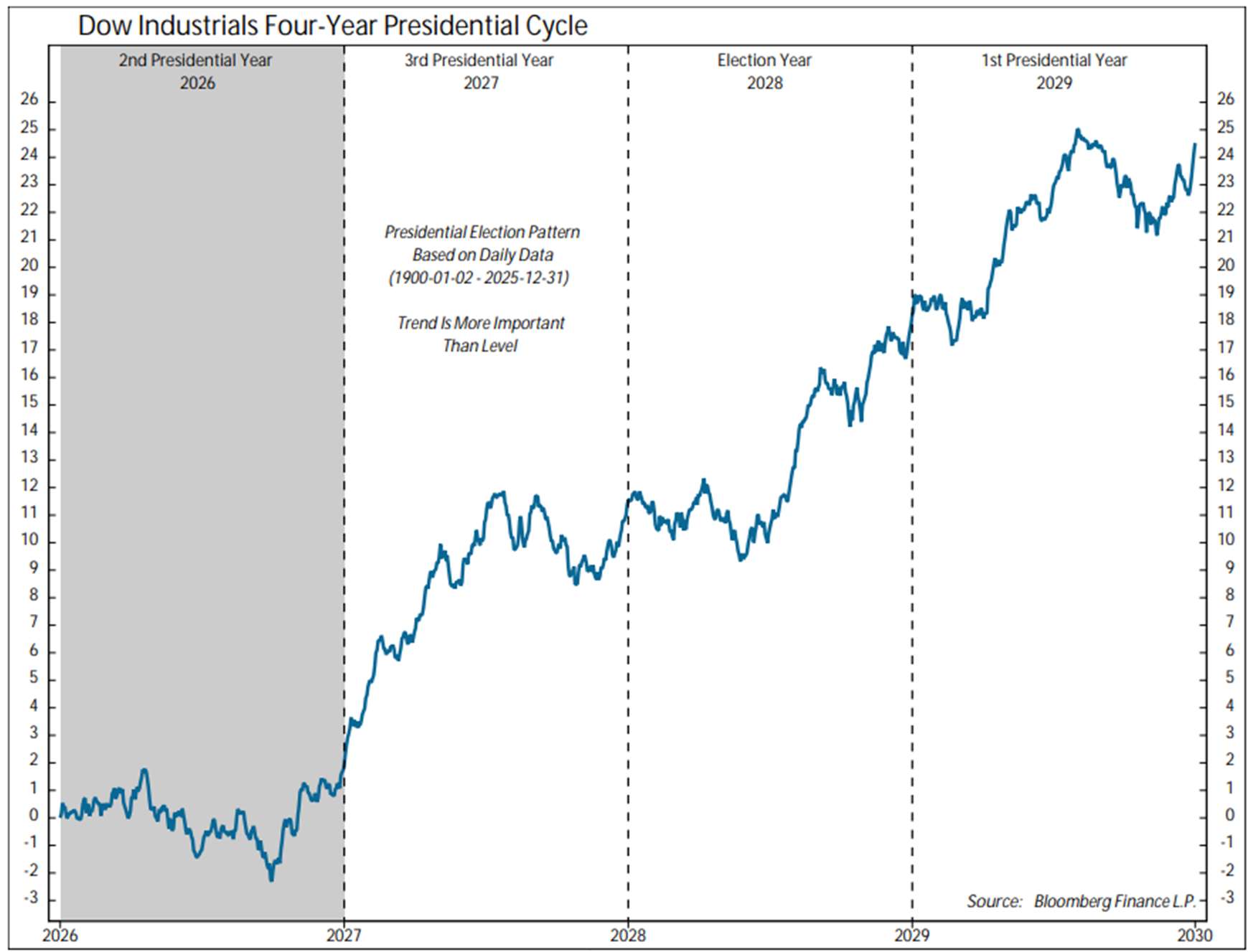

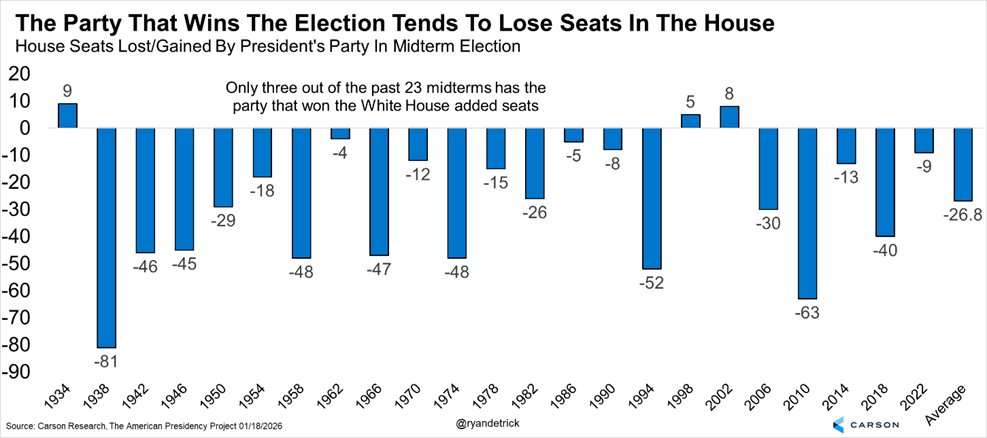

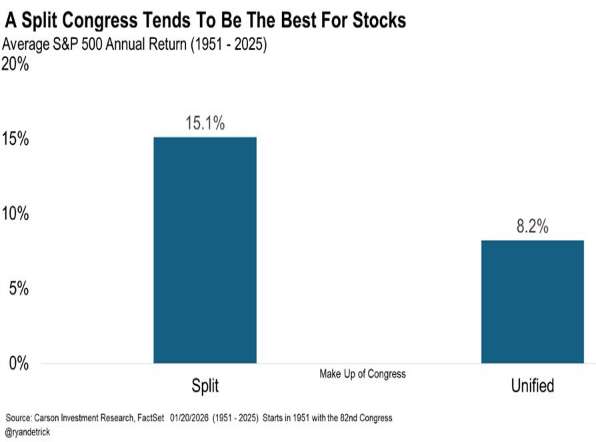

Mid-Term election years tend to be periods of consolidation. Policies enacted in the first year of the Presidential term are digested, and uncertainty rises with potential shifts in congress. Seats are typically lost by the Presidential party, and with the current tight majority it is likely we will move to a split House and Senate. But not to worry, subsequent years are empirically strong and a split congresses fares best for equity returns (Chart 7, 8). A pause should be welcomed to keep exuberance in check and allow valuations to moderate.

Performance in the quarter broadened and was driven by Small/Mid Cap and Value. Healthcare, Communications and Financials led as the AI spending was questioned and profitability fell into focus. Only Real Estate and Utilities were down, in response to rising rates. Technology, Industrials and Materials are likely to regain leadership as we move past year end rebalancing and attention returns to secular trends.

Important themes we are following are AI infrastructure and energy build out, emerging AI beneficiaries, reshoring of industry, increased defense spending and M&A. In addition, we are following emerging blockchain trends and government involvement in critical industries and materials.

Our playbook continues to focus on significant secular, cyclical, and structural trends. We favor highquality growth at reasonable prices and businesses with stable free cash flow and healthy balance sheets. We will continue to balance growth and value and are prepared to shift defensively if needed.

We remain in a secular bull market. Supported by the weight of evidence in economic growth, strong balance sheets, earnings, and ample liquidity. Mid-term election years tend to be choppy, but the tailwind of pro-growth policy and monetary easing continues to support a broadening of equity market returns and positive performance.

Robert B. Morse

Chief Investment Officer

1.

2.

3.

4.

5.

6.

7.

8.